For Internal use only. For external distribution, please use the document here.

Do you have a:

☑ Client who has held a share position for 10+ years with a substantial unrealized gain?

☑ Prospect who has exercised and holds a significant number of shares of their publicly traded employer?

Is diversification a concern, but the capital gains and the associated tax liability that would be triggered is a deterrent? What if the tax liability could be deferred, thus preserving and diversifying your client or prospects’ investment capital?

Section 85 “Transfer of Property to a Corporation by Shareholders” of Canada’s Income Tax Act (S.85 rollover) combined with Q Wealth’s TaxSmart Growth and Income Fund (TGIF) are a Q Wealth superpower and provide the means for clients and prospects to diversify an overweighted position tax efficiently. S.85 provides both a tax deferral and potential tax savings opportunity.

S.85 Rollover Explained

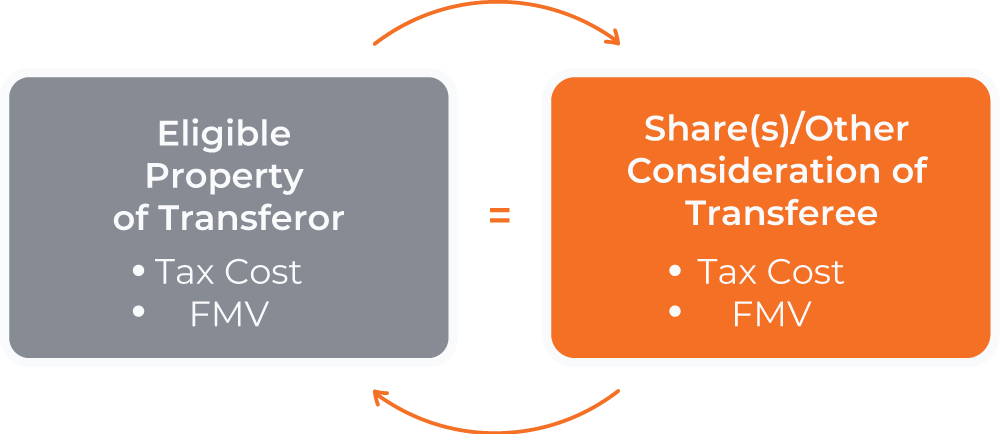

Normally upon the transfer of property from one taxpayer to another, there is a disposition at fair market value (FMV) and taxable gains are realized. However, a S.85 rollover allows an individual, a partnership, a trust or corporate taxpayer (transferor) to transfer eligible property to a corporation (transferee) without triggering an immediate taxable gain.

Eligible Property of the transferor could include capital property (such as land, building and investments), eligible capital property (such as intellectual property and goodwill), certain types of inventory and resource properties.

A S.85 rollover is made via a joint election by the transferor and transferee and sets out the exchange of the transferor’s eligible property for consideration from the transferor. The consideration must include at least one share of the transferor. Provided that the tax attributes of the transferee’s consideration are the same as the transferor’s eligible property, S.85 allows the exchange to be tax-free. The transferor, who is now a shareholder of the transferee, must be in the same economic position as before the exchange.

Note that there are additional variables to S.85 rollovers to consider, for example: the transferor may trigger income or capital gains in the exchange; and in addition to a share (or shares) of the transferee, debt or cash can also be received as consideration. Addressing these variables are beyond the scope of this communication, please speak to a tax professional to discuss further.

Sample Scenario

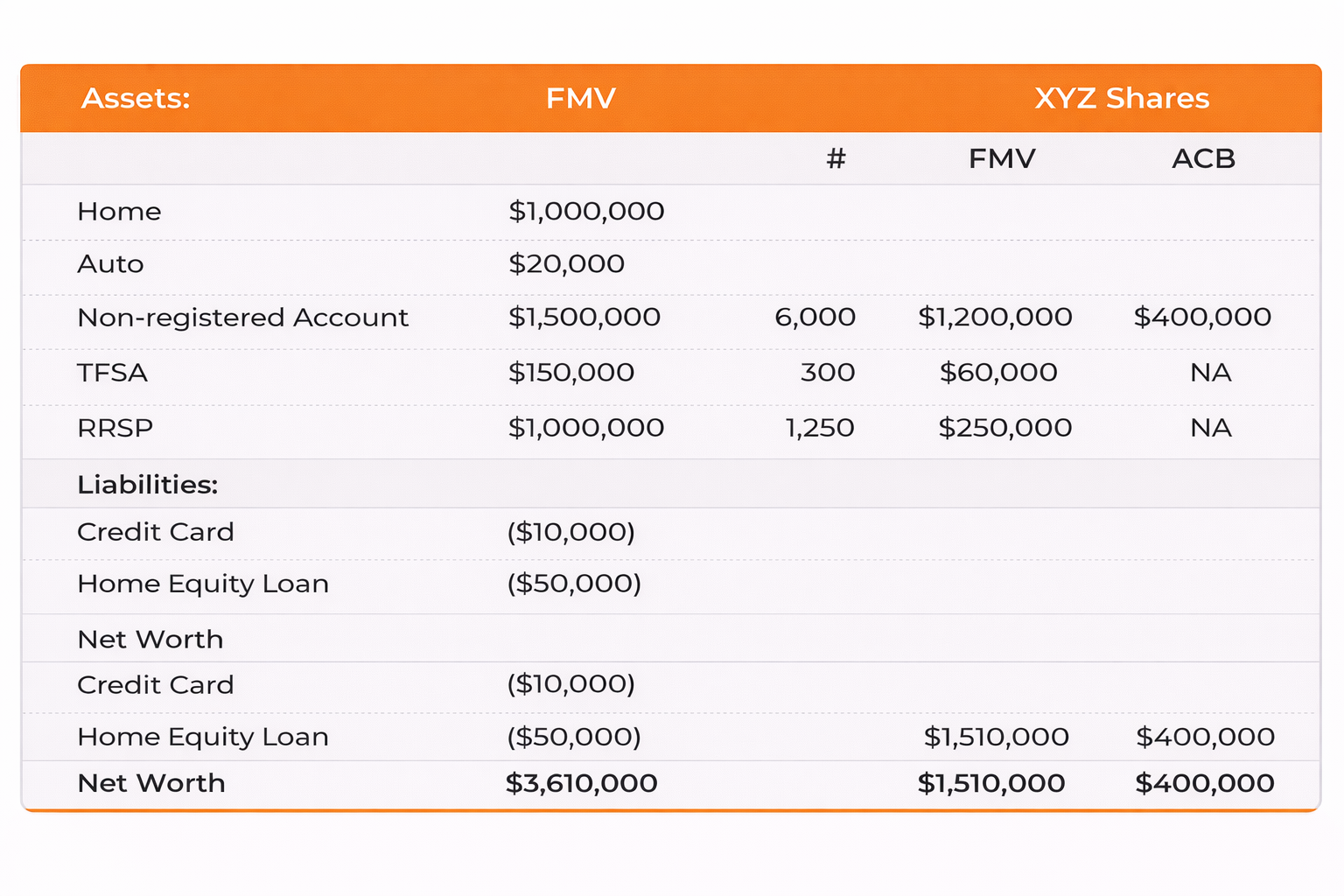

A prospect, Catherine Wong (55), has reached out to discuss her wealth planning needs. She has worked for a Canadian public company XYZ Co. the last 20 years and through share options, the employee share plan, and share splits she has amassed a significant amount of XYZ Co shares (XYZ shares). Her net worth (FMV) is as follows:

Big picture, Catherine’s income and benefits are tied to XYZ Co, and from her net worth standpoint, 41.8% is tied to her XYZ shares, or 57.0% if considering her investment assets only. She has expressed concern given her dependence on XYZ and has asked for recommendations.

Disposing the XYZ Co shares in her TFSA and RRSP accounts to diversity are straightforward, and no income taxes would be triggered. However, disposing of her XYZ shares in her non-registered account would trigger income taxes of approximately $200,000 (($1,200,000 - $400,000) * 50% capital gain inclusion rate * 50% combined personal tax rate). Catherine is taken aback her net worth would be reduced by $200,000 to diversify her non-registered investments.

A Tax Efficient Solution, Q Wealth’s TaxSmart Growth and Income Fund (TGIF)

TGIF is a corporate class mutual fund, meaning investors receive shares, not units of the fund.

Remember a key aspect of an S.85 rollover is at least one share of the transferee must be exchanged for the transferor’s eligible property.

Providing the Q Wealth Investment Team has approved the receipt of Catherine’s 6,000 XYZ shares held in her non-registered account, and to satisfy her wishes to have a 100% deferral/tax-free S.85 rollover, Form T2057 – Election of Disposition of Property by a Taxpayer to a Taxable Canadian Corporation, is completed by Catherine and Q Wealth.

The T2057 submission, would reflect the following in Schedule A Capital Property (shares only) section:

- Catherine exchanges her 6,000 XYZ shares with an ACB of $400,000 and FMV of $1,200,000 for

- TGIF shares with an FMV of $1,200,000.

Q Wealth’s back office would reflect the ACB of the TGIF shares in Catherine’s non-registered account received via the S.85 rollover at $400,000.

Catherine has maintained her net worth at the time of the exchange and her tax liability is deferred until such time she disposes of her TGIF shares.

Other S.85 Scenarios to Consider

Catherine used S.85 to diversify her investment holdings and defer the associated tax liability. S.85 can also be applied in scenarios such as estate freezes as part of a wealth transfer plan and corporate reorganizations involving the division of assets or departments into separate entities on a tax-efficient basis.

Connect with One Life Wealth Management

If you have a client or prospect that may be interested in engaging in an S.85 rollover using Q Wealth’s TGIF, please reach out to the Q Wealth Investment Team for an initial discussion.

For Internal use only. For external distribution, please use this document below.

.png)